Tax-Related Estate Planning

Introduction to Tax Planning

Advanced estate planning focuses primarily on reducing transfer taxes and income taxes. Under current federal law, there are three taxes that are imposed on the transfer of assets: the gift tax, the estate tax, and the generation-skipping transfer tax (“GSTT”). In addition to the transfer taxes that may apply, income tax can also reduce transfers. The gift tax applies to transfers made during life, the estate tax applies to transfers at death, and the generation-skipping transfer tax applies to transfers during life or at death that skip the children’s generation and pass to “skip persons”, who are generally grandchildren and those in lower generations.

- Gift Tax: A donor can give assets with unlimited values to spouses who are U.S. citizens and to qualified charities. In 2013 through 2017, gifts totaling up to $14,000 can be made to any number of individuals in each calendar year. In 2018, it is expected that the annual gift-tax exclusion amount will be $15,000. “Taxable gifts” are all gifts other than those that qualify for the (a) marital deduction, (b) charitable deduction, or (c) the annual exclusion; however, no out-of-pocket gift tax has to be paid until a donor’s cumulative lifetime gifts exceed the “applicable exclusion” (explained below) that is available for gift and estate tax purposes. After the applicable exclusion amount has been exceeded, the federal gift tax rate is 40% (during 2013 and beyond). The gift tax is paid by the donor out of assets remaining after the gift, so the tax itself is not included in the computation of the tax. (The annual exclusion was: $10,000 from 1997 to 2001; $11,000 from 2002 to 2005; $12,000 from 2006 to 2008; and $13,000 from 2009 to 2012.)

- Estate Tax: Upon death, the decedent’s gross estate includes the then current fair market value of all property interests held by the decedent at the time of his or her death, whether passing by operation of law (such as joint tenancy assets), by operation of contract (such as insurance proceeds), or by operation of probate laws. There are deductions for debts, administrative expenses, qualified transfers to spouses, and transfers to qualified charities. The net amount is the taxable estate. To the extent the applicable exclusion has not be utilized for lifetime gifts, it will be applied to the taxable estate. The estate tax is paid out of the taxable assets, so the amount of the estate tax itself is actually included in the computation of the tax.

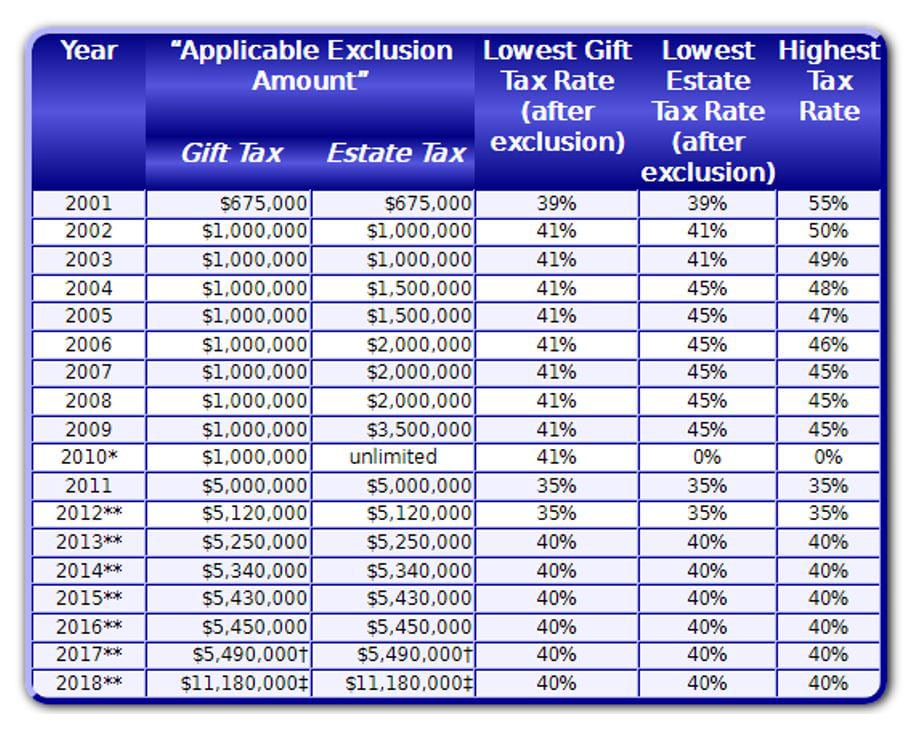

- Applicable Exclusion: The past, present, and future values for the “applicable exclusion” for the federal gift and estate taxes are shown in this table:

*The estate of a person who died in 2010 had the option to elect to either (1) pay no estate tax and be subject to a carryover basis for income tax purposes or (2) use the tax laws applicable to 2011, which provide for a $5 million applicable exclusion, a 35% tax rate, and a stepped-up income tax basis.

**The applicable exclusion for 2012 and beyond will reflect a “cost-of-living adjustment” from 2011. For 2018 and later, a “chained consumer price index” is used for cost-of living adjustments. Under the “portability” rules, the “applicable exclusion” for the federal estate tax may also include the applicable exclusion that the decedent’s predeceased spouse did not use IF the appropriate election is made on the estate tax return of the predeceased spouse.

†See Rev. Proc. 2016-55 for the 2017 figures.

‡As shown on page 18 of the “Overview of the Federal Tax System as in Effect for 2018” published in February of 2018 by the Congressional Joint Committee on Taxation.

- Generation-Skipping Transfer Tax: Congress enacted the generation-skipping transfer tax (GSTT) which applies to transfers to “skip persons”, whether made during life or at death. “Skip persons” are grandchildren and lower generations. The GSTT is a one-rate tax equal to the highest applicable estate tax rate (shown in the table above this paragraph), and it applies in addition to any applicable gift or estate tax. Estate taxes paid are deducted before computing the GSTT, but combination of the estate tax and the GSTT can result in a combined rate of over 70%. Each donor or decedent has a $5 million GST exemption (adjusted for inflation in 2012 and beyond), which can be used for transfers either during life or at death. The GST exemption applies to the transferor (donor or decedent) regardless of the number of skip persons to whom the transfers are made. Since 2004, the GST exemption has been the same as the “applicable exclusion” for estate tax purposes. The GST exemption is not “portable” from the spouse who dies first to the surviving spouse.

- Income Taxes: Income taxes further deplete transfers, especially with respect to assets that are all taxable income, such as retirement plan benefits. The combination of transfer taxes and income taxes can deplete some transfers by more than 85%.

Nontax Issues

- Nontax Goals: A will or a living trust can accomplish most of your nontax objectives. First, you want to make sure that your assets are administered and distributed as you desire. Second, you want to minimize the expenses and complications that can come with the administration of your estate. The primary tool for most clients with substantial estates is the revocable living trust. A properly drafted living trust can be used to:

- Provide for your own care and benefit during any periods of incapacity without the need for guardianship proceedings;

- Make sure that assets are transferred after your death to your intended beneficiaries;

- Reduce or perhaps eliminate the need for probate proceedings at death, together with the fees, costs, and delays associate with probate;

- Protect beneficiaries from mismanagement and from the claims of creditors and ex-spouses;

- Discourage certain types of conduct; and/or

- Give incentives to beneficiaries to be productive members of society.

Basic Transfer-Tax Planning

- Revocable Trusts: Revocable trusts can be structured to reduce and/or defer the estate tax and the generation-skipping transfer tax, especially for married couples. In other words, revocable trusts can be used to:

- Defer estate tax for married couples upon the death of the first spouse to die through the use of marital-deduction trust planning.

- Reduce or eliminate estate taxes for beneficiaries by establishing one or more “bypass trusts”.

- A bypass trust can be used as a “credit-shelter trust” to preserve a decedent’s estate tax “unified credit” or “applicable exclusion”, which is $5,000,000 in 2011 and 2012. [For other years, see the applicable exclusion table, above.]

- A bypass trust that maximizes the GST exemption can also serve as a “generation-skipping trust” to reduce or eliminate estate taxes for children and other descendants.

Bypass Trust

- Generally: A “bypass trust” is used to give benefits to one or more beneficiaries without giving them enough rights of ownership to require taxation of the trust assets in the beneficiaries’ estates. A bypass trust can also qualify as a “spendthrift trust” which is not subject to the claims of creditors, including judgment creditors, which is useful even when transfer taxes are not a concern.

- Permitted Benefits: The Internal Revenue Code permits a beneficiary to receive significant benefits from a trust without causing the trust or its assets to be considered part of the beneficiary’s estate. Unless the assets were contributed by the beneficiary, the assets will not be considered part of the beneficiary’s taxable estate if even the beneficiary has the right to:

- Receive all trust income.

- Receive payments from trust principal for support, health, education, and maintenance.

- Withdraw 5% of principal per year.

- Direct distributions of the principal during life (to recipients other than the beneficiary and the beneficiary’s creditors)

- Direct distributions of the principal after death (to recipients other than the beneficiary’s estate or creditors)

- Act as a trustee.

- Maximum Benefits Bypass Trust: A trust which gives a beneficiary all of those rights is often referred to as a “maximum-benefit bypass trust”. A maximum-benefit bypass trust gives most of the flexibility that would come from outright ownership without subjecting the assets to the claims of creditors, the claims of disgruntled spouses in a divorce proceeding, or the obligation to pay federal estate taxes.

- Additional Restrictions: Not every bypass trust needs to be a maximum-benefit trust, and the settlor can restrict or eliminate any or all of the powers. It is common, for example, to eliminate the annual 5% withdrawal right and to limit the power to direct distributions so that the recipients must come from a particular group, such as the settlor’s descendants.

- Bypass Trusts for Spouses: For married couples, it is common to want to shelter the predeceased spouse’s applicable exclusion1 while at the same time leaving the surviving spouse with broad benefits and control over the exempt amount. Perhaps the “Credit-Shelter Trust” is the most common form of the bypass trust, and it is discussed briefly below.

- Bypass Trusts and the GSTT: Before the enactment of the generation-skipping transfer tax (GSTT), there was no restriction on the value of assets that could be allocated to a bypass trust. Under current law, up to $5 million can be allocated to a bypass trust without incurring the 40% GSTT at one time or another.

- For any person who names a grandchild as a beneficiary or as an alternate beneficiary, it is important to allocate as much as possible into a totally exempt trust so that all federal transfer taxes can be avoided.

- Although a bypass trust can always save the federal estate tax, it cannot save the GSTT unless the trust is totally exempt. Unlike the estate tax, the GSTT has no lower tax brackets, so it is usually unwise and unnecessary to incur a generation-skipping tax.

- A trust is made exempt from the GSTT by filing a federal gift tax return (IRS Form 709) each time transfers are made to it and by declaring on the return that the GST exemption equal to the value of the transfers is allocated to the trust. After death, the GST exemption is claimed on the federal estate tax return (IRS Form 706).

The A/B Trust and the A/B/C Trust

Any two persons (“settlors”) can create an “A/B Trust” or an “A/B/C Trust”. This type of trust begins as a single revocable trust, but when one of the settlors dies, the trust divides into subtrusts.

- A/B Trust: Upon the death of the first settlor to die, an A/B Trust divides into Trust A and Trust B.

- “Trust A” or the “Survivor’s Trust” remains revocable and contains the survivor’s property interests, and the surviving settlor has total control. If the survivor is the deceased settlor’s spouse, this trust usually receives all assets that exceed the applicable exclusion, and this qualifies for the marital deduction, thus deferring any estate tax until the surviving settlor’s death. If the survivor and the deceased settlor are not married, the deceased settlor’s assets are usually not added to the survivor’s trust since there is no way the transfer can qualify for the marital deduction.

- Trust B or the “Credit-Shelter Trust” is irrevocable. It is designed as a bypass trust, which is discussed above. For a married couple, the Credit-Shelter Trust contains the deceased settlor’s assets that can pass tax free, equal to the unused applicable exclusion. For a married couple, this trust contains the deceased settlor’s assets, and the estate tax is imposed on the trust to the extent it exceeds the applicable exclusion. This trust is designed as a bypass trust so that it can pass to the next generation of beneficiaries without triggering a transfer tax.

- A/B/C Trust: Upon the death of the first settlor to die, an A/B/C Trust divides into Trust A, Trust B, and a Trust C. This type of trust is frequently used for a married couple whose combined estate exceeds double the applicable exclusion. This structure is rarely used for unmarried persons because federal law does not allow a marital deduction for unmarried persons, and federal law does not recognize a civil union or a domestic partnership as a marriage.

- Trust A or the Survivor’s Trust contains the surviving settlor’s assets only.

- Trust B or the Credit-Shelter Trust contains the amount that can pass free, which is equal to the unused applicable exclusion.

- Trust C is a Marital Trust, which qualified for the marital deduction.

- The most common type of marital trust is the “qualified terminable interest property trust”, which is referred to as a QTIP Trust. In this type of trust:

- the surviving spouse must be entitled to receive all of the trust’s income during the survivor’s lifetime;

- the surviving spouse must be able to compel the trustee to make unproductive assets produce income; and

- no one but the surviving spouse may be a beneficiary until after the surviving spouse’s death.

- Another type of marital trust is the “income-and-general power of appointment” trust. In this type of trust:

- The surviving spouse must be entitled to all of the the trust’s income during the survivor’s lifetime;

- the surviving spouse must be able to compel the trustee to make unproductive assets produce income; and

- the surviving spouse must have a “general power of appointment” that permits the survivor to say where the trust goes upon the survivor’s death. A “general power of appointment” is one that is exercisable in favor of the survivor, the survivor’s estate, the survivor’s creditors, and/or the creditors of the survivor’s estate.

- The QTIP is frequently used because:

- This is considered a spendthrift trust in many jurisdictions, which means it is not subject to the creditor’s of the surviving settlor.

- The trust may restrict the surviving settlor from making changes, making it appropriate where each spouse has different beneficiaries, such as children from prior marriages.

- A portion of the QTIP trust can be made exempt from the generation-skipping transfer tax (GSTT) using the GST exemption of the first spouse to die.

“Portable” Applicable Exclusion for Spouses. Under the 2010 Tax Relief Act, a credit-shelter trust is not required to preserve the applicable exclusion that not used by the predeceased spouse. The unused applicable exclusion can apply to the surviving spouse’s estate. Even so, because the credit-shelter trust provides asset protection and because remarriage can eliminate the ability to use the prior’ spouse’s credit, it is usually advisable to use a credit-shelter trust.

Qualified Domestic Trust. A “qualified domestic trust” or “QDT” (pronounced “Q-dot”) is a marital trust that has a U.S. Trustee and meets other requirements imposed by law to assure that the estate tax will be paid. If the surviving spouse is not a citizen of the United States, a marital trust will not qualify for the marital deduction unless the marital trust complies wth the QDT requirements.

The Need to Go Beyond the Basics

- Saving Transfer Taxes: Revocable trusts cannot eliminate estate taxes for unmarried individuals with estates exceeding the applicable exclusion or for married couples with estates exceeding twice the applicable exclusion ($10,500,000 in 2013). In those cases, transfer taxes must be provided for in one way or another. Either the taxable estate must be reduced, or arrangements must be made to pay the tax. There are many estate planning “tools” that can use to supplement your basic will and/or revocable trust. The purpose of these materials is to briefly outline some of those tools.

- Personal Considerations: Most of the estate-tax savings techniques require you to give up at least some control over your own assets and to limit or eliminate the benefits you receive from them. Only you can decide how much benefit and control you are willing to give up in order to save someone else (your children or other beneficiaries) taxes and other expenses at a future date.

- Some techniques — like life insurance trusts — probably will not have much impact on you or your lifestyle because you are giving up control over and benefits from an asset you probably would not tap into anyway. Of course, if your planning requires significant insurance, it will also require the payment of significant insurance premiums, making cash flow an important factor in your estate plan.

- Some estate planning tools seem illogical and can simply make people uncomfortable. For example, irrevocable trusts can be designed so that the grantor*.does not receive trust income but pays income taxes on trust income in order to indirectly benefit trust beneficiaries without making taxable gifts. It may be psychologically unpleasant to have to pay taxes on someone else’s income, but for persons trying to reduce their taxable estates, it can be an effective tool.

- Other techniques — such as a qualified personal residence trust — require you to give away assets earlier than you normally would, assets that you may really want to keep and use for the rest of your life.

- And some techniques — such as charitable remainder trusts — not only remove assets from your estate, but also keep those assets from your children or other beneficiaries.

- Each person has to decide for himself or herself the combination of estate-planning techniques that balance the desire to save taxes and expenses with the desire to maintain control over and benefits from hard-earned assets.

These materials continue in the article entitled “Reducing the Taxable Estate”.

*NOTE: “Grantor”, “settlor”, and “trustor” are used interchangeably to refer to the creator of a trust.

Attorneys

Our experienced attorneys can help with your estate planning needs.